What PE firms typically do once they buy into a legal tech software vendor, why they do it, and where customers can get burned.

|

Playbook Step

|

What PE Sponsors

Actually Do

|

Legal-Tech

Examples

|

Customer-Side

Risks & Harms

|

|

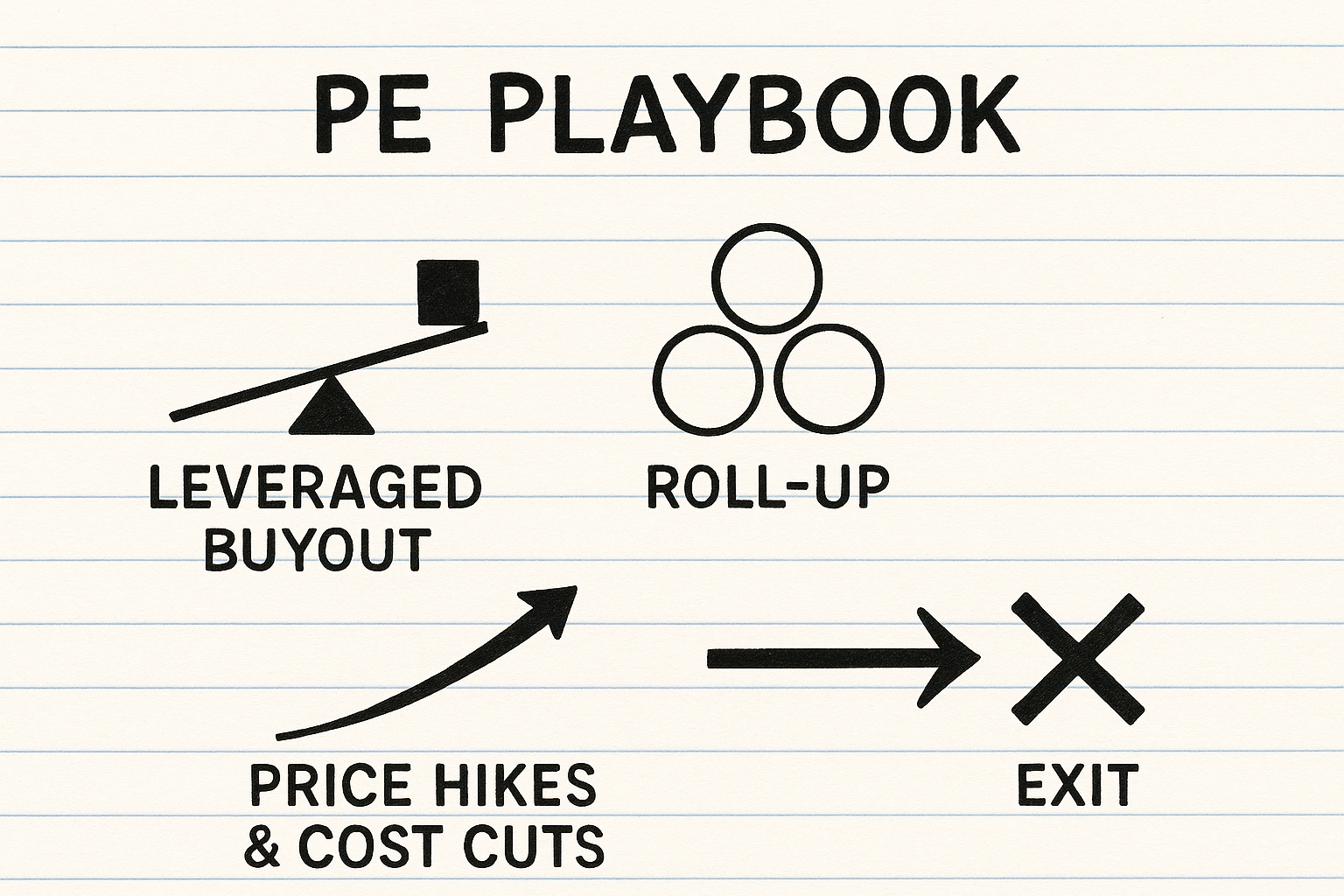

1. Buy with Leverage

|

Use 50-70 % debt to fund the deal and load that debt on the target’s balance sheet.

|

• Warburg Pincus & Cove Hill recap NetDocuments in 2021 (undisclosed purchase price).

• Hg takes Litera private in 2019, funds 10+ bolt-ons with unitranche debt.

|

High fixed debt service → pressure to cut costs (support, R&D) and raise prices.

|

|

2. Roll-up Bolt-ons

|

Acquire direct competitors or adjacent workflow tools, then collapse them into one platform to grow ARR fast.

|

• NetDocuments → Worldox (Oct 2022) adds 6,000 SMB firms in one shot. LawSites

• Onit (K1, $200 M) buys SimpleLegal (2019), BusyLamp (2021), Bodhala (2022). Onit

|

• Forced migrations (Worldox desktop → NetDocs cloud). LexWorkplace reports higher TCO and data-conversion fees. LexWorkplace

|

|

3. Raise List Prices & Retire “Overlaps”

|

After integrations, sunset duplicate SKUs, impose subscription-only licensing, and embed annual uplift clauses (+7–12 %).

|

• Litera ends support for Workshare Compare & DocsCorp suites, pushing firms to new Litera bundles. Innovative Computing Systems, Inc.Legal IT Insider

|

• Price hikes during renewal; customers pay to re-train staff or re-platform.

|

|

4. Cut SG&A to expand EBITDA

|

Trim overlapping marketing & support teams to hit the 20–30 % EBITDA margin PE funds expect.

|

• Litera cut AUS marketing & product staff after DocsCorp acquisition. Legal IT Insider

|

• Reduced regional support windows; slower bug-fix cycles.

|

|

5. Cross-sell & Bundle

|

Use the new, larger install base to upsell add-ons (e-billing, contract AI) and squeeze more ARR per customer.

|

• Onit bundles Bodhala spend analytics with SimpleLegal mid-market ELM.

• NetDocuments sells ndThread & CollabSpaces to Worldox converts.

|

• Increased vendor lock-in; switching costs escalate as more workflows sit in one stack.

|

|

6. Refinance or Exit in 3–7 yrs

|

Sell to another PE firm, list via IPO, or flip to a strategic—pocket the multiple expansion.

|

• Silver Lake buys into Relativity at a $3.6 B valuation (2021) and will seek a 2–3× return at exit. Built In Chicago

|

• Another owner can restart the cycle—new debt, new price schema, new road-map priorities.

|

Why PE likes legal tech

- Sticky revenue: Once mission-critical data (contracts, work product) is inside a platform, churn is <5 %.

- Highly fragmented market: Easy to bolt-on smaller vendors and create scale economies.

- Pricing power: Law-firm & corporate legal budgets are still a small slice of total matter value, giving head-room for increases.

Customer risks in detail

- Price inflation outpacing value.

Post-deal list prices often jump 8-15 % at the first renewal; some firms report a 40 % TCO hike moving from Worldox to NetDocuments’ cloud LexWorkplace

- Forced migrations & product sunsets.

Litera’s EOL notices give <24 months before legacy Workshare/DocsCorp tools stop patching security bugs. Innovative Computing Systems, Inc.Litera

- Support degradation.

Lay-offs of regional teams (e.g., Litera Australia) mean slower ticket response and fewer local experts. Legal IT Insider

- Innovation stall.

Debt service + EBITDA targets redirect cash from R&D to interest payments, delaying needed features (e.g., Worldox users waited years for modern cloud search).

- Change-of-control uncertainty.

When Silver Lake exits Relativity, a new owner could split cloud vs. on-prem SKUs or spin-off analytics—customers have no seat at that table.

Mitigation checklist for buyers

|

Clause / Action

|

What it Protects Against

|

|

Price-cap clause: max CPI+2 %

|

Shields against post-buyout hikes.

|

|

Change-of-control opt-out

|

Right to terminate or demand free migration if ownership changes.

|

|

Road-map escrow / source-code escrow

|

Coverage if acquirer sunsets or pivots the product.

|

|

Support-staff SLA (FTE ratio)

|

Prevents aggressive head-count cuts from crippling service.

|

|

Data-export in open standard (JSON, XML)

|

Lowers switching cost if PE roll-up forces an unwanted bundle.

|

Key take-away

Investor-owned platforms can deliver real scale and innovation—but the PE playbook (debt, roll-ups, price lifts, support cuts) creates predictable customer pain points. Write strong contract clauses (price caps, change-of-control escape, support SLAs, open-data export) and keep an eye on ownership news so you’re protected before a deal closes.

Add one more lever—look beyond the funded crowd.

Bootstrapped or family-owned vendors such as LEAP (small-firm PMS), Dennemeyer (global IP management), mot-r (legal work orchestration) and long-standing niche tools like Tabs3 often:

- price more predictably (no EBITDA targets to hit),

- maintain stable road-maps for decades, and

- offer direct access to founders for support.

Including at least one “un-funded” alternative in every RFP keeps pressure on PE-backed suppliers—and gives you a fallback if the next roll-up cycle makes your current vendor too expensive or too risky.